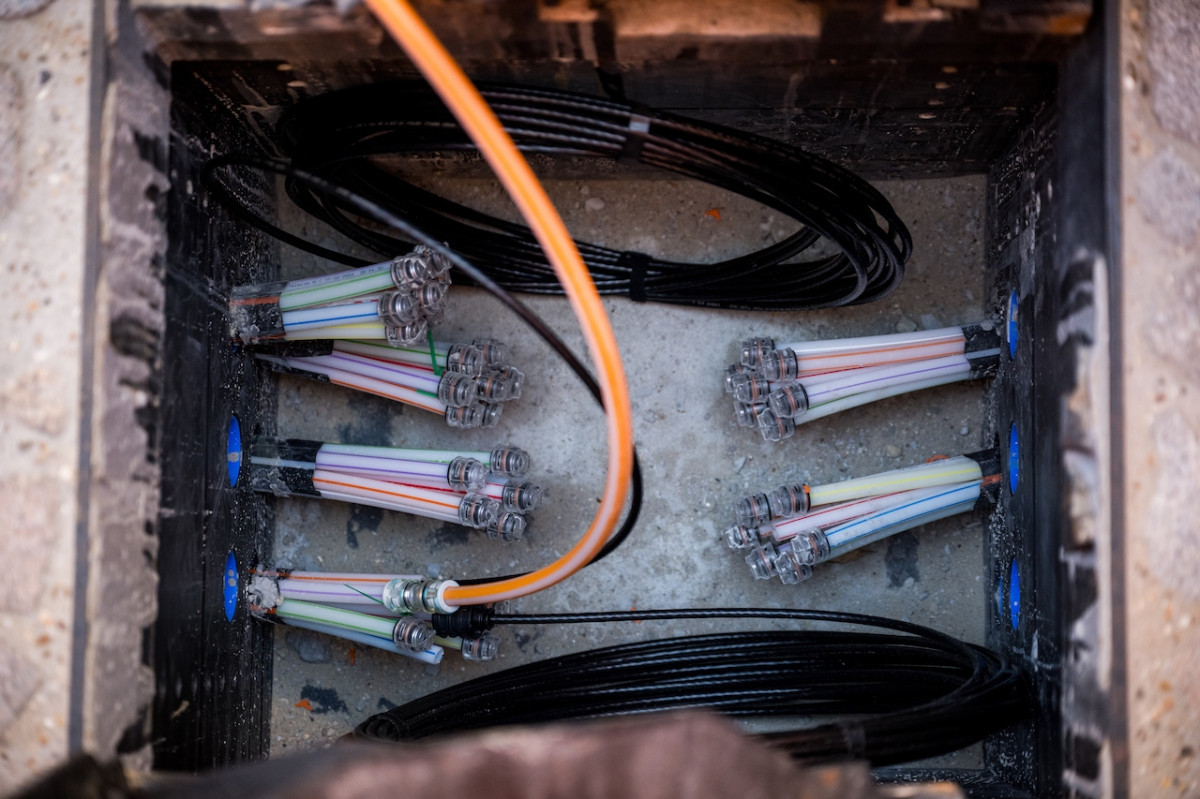

Between European technology policies there are several success stories. One of them is the deployment of fiber optic networks in Spain. Today, the country boasts a coverage that reaches 96% of households and 99.7% of the population, placing it ahead of powers such as Germany or the United Kingdom.

However, behind this remarkable rollout, complex regulatory debates are emerging. In the offices of the National Commission on Markets and Competition (CNMC) — and in the corridors of Brussels — the focus is no longer solely on connecting more citizens, but on the sustainability of networks in the present and, above all, in the future. At the heart of the discussion is the MARCo regulation (Access to Records and Conduits), the rule that obliges the incumbent operator, Telefónica, to cede its civil infrastructures to competitors at regulated prices.

This measure began in 2009, conceived then as an emergency option to avoid unnecessary trench duplication and accelerate competition. But today it threatens to become an anchor for investment in the sector and poses a question: does it make sense to apply the 2009 regulatory logic to one of Europe’s most competitive markets in 2026?

An unrecognizable market and the myth of the “natural monopoly”

When MARCo regulation was born nearly two decades ago, alternative operators hardly had any private network of their own. Regulators’ objective was clear and justified: facilitate access to existing conduits and poles to energize a stagnant market.

That objective was successfully achieved. Industry estimates suggest that using these shared infrastructures allowed competitors substantial savings, ranging from 60% to 80% of their total deployment costs. Therefore, thanks to this policy, Spain attracted capital, democratized high-speed connectivity, and greatly reduced the rural digital divide.

“Industry estimates suggest that using these shared infrastructures allowed competitors substantial savings, ranging from 60% to 80%”

Nevertheless, yesterday’s success could become today’s burden. Some sector players insist on clinging to the idea that Spain’s civil infrastructures constitute a “natural monopoly”. In light of this hypothesis, a look at 2026 market data shows that the situation is far from that proposed scenario.

Spain is probably the European country with the greatest number and quality of alternative civil infrastructures. Beyond Telefónica’s network, there are robust options:

- Cable networks: the legacy infrastructures of cable operators, now integrated into giants like MasOrange and Vodafone, covering more than ten million households.

- Third-party infrastructures: there exists a vast network of usable conduits from other sectors (energy, water, gas) and civil works by public administrations, whose capillarity rivals that of the incumbent itself.

Consequently, it would be misguided to speak of a natural monopoly in a country with hundreds of networks and record levels of competition. Moreover, updating MARCo does not mean restricting access or altering competition guarantees, but gradually revising the economic terms to better reflect the current costs of operation, maintenance, and investment.

Capital at risk

One of the most repeated mantras by those who oppose updating access prices is that Telefónica’s infrastructures are merely a legacy from the era of state monopoly prior to 1998. Yet this is a sector that has already undergone more than a quarter of a century of market economics.

Since liberalization, Spain’s housing stock has added more than 7.5 million new homes. To connect these urban developments, as well as the vast and complex rural Spain, tens of billions of euros in purely private investment have been required. Moreover, the civil network is not a rigid block of concrete. Rather, it can be described as a living ecosystem. Wooden poles rot, conduits may collapse or suffer damage from third-party works, and manholes require constant maintenance.

“The civil network is not a static block of concrete. It is a living ecosystem”

“It cannot be expected to invest massively in strategic infrastructures while regulatory frameworks designed for another technological cycle are maintained indefinitely”, warn EU telecom investment analysts. Maintaining this capillarity implies rising operating costs. In this sense, the current model perpetuates an asymmetric value transfer: the entity that maintains the network bears the risk and inflationary spending, while third parties exploit the same infrastructure at artificially depressed prices due to regulation.

The paradox of reciprocity and market prices

That is the narrative concerning monopoly. To respond to the argument of “fair prices,” it is necessary to analyze the reciprocity of the Spanish market.

Certain alternative operators have repeatedly warned that any adjustment of MARCo prices by the CNMC would jeopardize their investments. In contrast, the practices within operator relationships tell a very different story. There are cases where the flow is reversed and Telefónica needs to rent space in the infrastructures of these competitors. When this happens, the rates applied to Telefónica are certainly not “regulated”.

“Certain alternative operators have insisted that any adjustment of MARCo prices by the CNMC would risk their investments”

Market sources confirm that other operators charge the Spanish company multiples that can reach doubling, quadrupling, or even tenfold the price they themselves pay to use the MARCo network. It is untenable to argue that a regulated price is “abusive” or harmful to competition when the same operators charge drastically higher prices for an identical service.

Sovereignty and European resilience enter the debate

The discussion about conduits in Spain occupies only a few cells of the entire strategic framework confronting Europe. The continent pursues ambitious objectives: strategic autonomy, digital resilience against cyber threats, the infrastructure needed for the AI revolution, and modernization of critical networks. As one would expect, all of this requires capital. A lot of capital.

The European legislative framework itself, through the recent Gigabit Infrastructure Act, has already begun to steer the course. Brussels’ directive is that providers who facilitate access to their physical infrastructures must have a fair and reasonable opportunity to recover the costs incurred. Therefore, the European regulator has understood that excessive impositions on the network builder undermine the incentives to keep upgrading it.

“Updating regulated prices in Spain does not equate to a ‘remonopolization,’ as the more alarmist voices warn”

In this regard, updating the regulated prices in Spain does not equal a “remonopolization,” as the alarmist voices claim. No one, in any institution, is questioning the right of third parties to access these conduits. Technical and operational access will remain fully guaranteed. The conversation is shifting toward a gradual application and adjustment of tariffs to the current economic reality, moving away from the de facto subsidy represented by prices below cost.

Adapt or stagnate

At this juncture, some critics argue that price increases would slow deployment. Let’s look at the numbers. Data indicate that the cost of renting conduits today represents a marginal portion of the total fiber deployment costs for any mature operator. The networks are already in place, public deployment funds (such as the ÚNICO program) are nearing completion, and the market is highly consolidated.

In this context, one could argue that legal uncertainty does not come from updating a price, but from keeping a regulatory framework static while the economy, inflation, and technology advance. Tariff reviews—whether increases or decreases—are a normal and healthy tool in any market democracy. In fact, the CNMC’s own data suggest that even with adjustments, regulated prices remain below actual costs recognized.

“Maintaining the 2026 ecosystem under the same rules no longer fixes a market failure and may even create others”

Spain achieved its fiber leadership thanks to a bold and interventionist regulation in 2009 that addressed a market failure. Keeping the 2026 ecosystem under those same rules no longer fixes a market failure and may even create others. If Europe wants its operators to have the financial muscle to compete in the era of artificial intelligence and to safeguard its critical infrastructures, it must ensure that its regulation continues to incentivize those who invest, maintain, and modernize critical infrastructure.

The success of fiber in Spain is now history. It’s time to start financing the future.