Access to critical materials has become a central axis of global geostrategic competition, profoundly reshaping international relations and power dynamics. China dominates the refining of rare earths with more than 85% of world capacity and processes about 80% of the cobalt mined worldwide, giving it decisive leverage over strategic sectors such as the energy transition, the tech industry, and defense. This dominance is not accidental: it results from decades of strategic investment and long-term planning by Beijing, which has made the control of critical-material value chains a cornerstone of its industrial policy and national security.

“Trump has reactivated rare-earth mines in Texas and California, with the ambitious aim of reducing China dependence by 40% by 2030”

The Trump Administration has significantly intensified its efforts to counter this Chinese dominance and strengthen American autonomy in the supply of critical materials. After returning to the presidency in 2025, it has enacted an aggressive incentive program to reactivate rare-earth mines in Texas and California, with the ambitious goal of cutting dependence on China by 40% by 2030. This program includes not only direct subsidies for production but also massive investments in research and development of processing technologies. The response from Beijing has been forceful: new restrictions on the export of key metals and the strengthening of its grip on global supply chains.

Click on the map to zoom. Map: Cassini España

The map shows the global strategies to secure critical mineral supply, highlighting the main exporters and their policies. China leads the sector, while the United States, the EU, and Australia seek to reduce dependence through strategic reserves and agreements. Also identified are countries with export-restriction plans, reflecting the rising competition for these resources essential to the energy transition and technological advancement.

In this context of growing trade tensions, Greenland has emerged as a key strategic territory. Its vast reserves of rare earths, especially at the Kvanefjeld deposit, have unleashed intense geopolitical competition. Denmark has systematically blocked attempts by China to gain influence on the island, from the thwarted purchase of the Grønnedal naval base in 2017 to the rejection of Chinese firms’ airport modernization plans in 2019. The 2023 decision by the autonomous Greenlandic government to reject the exploitation of Kvanefjeld, where Greenland Minerals operated with Chinese participation, illustrates the complexity of balancing economic, environmental, and geopolitical interests.

The Lithia Triangle faces a structural dilemma: despite its resource wealth, a lack of technological capabilities and refining infrastructure preserves dependence on major global buyers

Beyond the Arctic, Latin America and Africa have emerged as crucial stages in this new geography of critical materials. The Lithium Triangle, formed by Argentina, Bolivia, and Chile, hosts more than 55% of the world’s reserves of this mineral, indispensable for electrifying transport and storing energy. Yet the region confronts a structural dilemma: despite its resource riches, the lack of technological capacity and refining infrastructure sustains reliance on large consumer powers. China and the EU are aggressively competing to secure long-term supply contracts, anticipating demand that, according to projections from the International Energy Agency, could rise by 500% by 2030. This dynamic mirrors historic patterns of dependence, albeit with new players and technologies.

Africa, for its part, plays a crucial role in cobalt production, though its market remains markedly asymmetrical. The Democratic Republic of the Congo, which extracts about 70% of the world’s cobalt, epitomizes the contradictions of today’s critical-materials system. China has established near-monopoly control over the refining and marketing of this strategic mineral, essential for electric-vehicle batteries and other advanced technologies. This dominance has been built through decades of investment in infrastructure and favorable trade agreements. This dependence worries the West, as it constrains the ability to diversify supply sources. Moreover, working conditions in Congolese mines and the lack of regulation have sparked controversy, reinforcing the need to set more sustainable standards across the supply chain.

For the European Union and the United States, the high geographic concentration of these strategic resources presents multiple challenges. European dependence is not limited to China for rare earths; it also extends to Russia and South Africa for platinum-group metals, essential for clean-energy technologies and advanced industrial applications. The vulnerability of these supply chains became evident between 2021 and 2023, when the price of lithium quintupled due to geopolitical disruptions and production bottlenecks. This episode demonstrated how market volatility can directly affect the viability of the energy transition and industrial competitiveness.

The United States has attempted to address these vulnerabilities through the 2022 Inflation Reduction Act, which allocates $369 billion to reindustrialize the critical-materials sector. However, rebuilding decades of offshored industrial capacity faces significant obstacles: from shortages of skilled labor to the need to develop new environmentally sustainable processing technologies. The American experience underscores the complexity of reversing strategic dependencies once established.

This global panorama shows that competition for critical materials has transcended mere economics to become a determining factor in 21st-century geopolitics. For the European Union, the challenge is particularly acute: it must balance its pursuit of strategic autonomy with the reality of a market dominated by established players, while ensuring that its energy and digital transition is not jeopardized by disruptions in the supply of essential materials.

The European response: Critical Raw Materials Act (CRMA)

In the face of growing supply vulnerabilities and geopolitical tensions, the European Union has framed an ambitious response through the Critical Raw Materials Act (CRMA) of 2023. This legislation marks a turning point in Europe’s industrial policy, establishing for the first time binding quantitative targets: achieving 10% internal extraction of critical materials and 15% sourced from recycling processes by 2030. Yet the CRMA goes beyond numeric aims; it represents a fundamental reconceptualization of Europe’s strategic autonomy in the era of energy transition and digitalization.

“The EU has recognized that the real vulnerability lies not only in extraction, but in the ability to transform these materials into high-value components”

The first pillar of the European strategy focuses on strengthening the bloc’s internal capabilities. This includes not only identifying and developing strategic deposits, such as lithium in Extremadura or rare earths in Sweden, but also building a comprehensive processing and refining infrastructure. The EU has recognized that the real vulnerability lies not only in extraction but in the ability to transform these materials into high-value components. To address this gap, substantial funding has been allocated through the Horizon Europe program and the Innovation Fund to develop advanced, environmentally sustainable processing technologies.

The building of strategic international partnerships constitutes the second fundamental pillar. The Partnership on Critical Minerals with Canada, established in 2022, has emerged as a model of collaboration based on high environmental and social standards. This agreement not only secures access to nickel and cobalt but also establishes a framework for joint research and development of sustainable processing technologies. Australia has become another crucial partner, especially in the realm of rare earths, where joint projects aim to develop alternatives to China’s dominance in refining. In Africa, agreements with Namibia and the Democratic Republic of the Congo represent a new approach that emphasizes local capacity development and the implementation of sustainability standards.

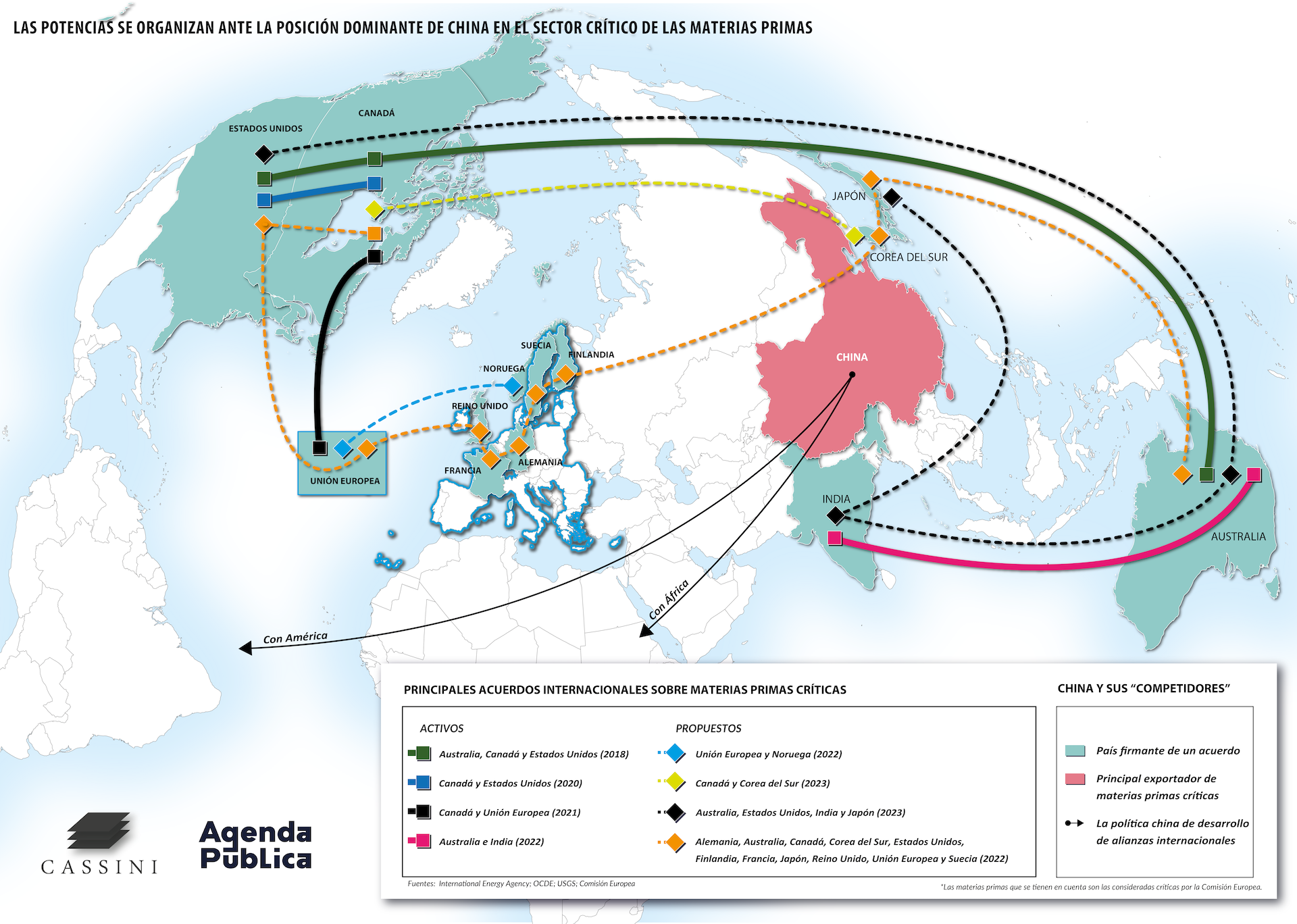

Click on the map to zoom. Map: Cassini España

The map highlights the main international agreements on critical raw materials as a response to China’s dominant position in this sector. It emphasizes cooperation among countries such as the United States, Australia, Canada, the EU, Japan, and South Korea, which have signed strategic agreements since 2018 to diversify their supply sources. It also reflects China’s alliances with Latin America and Africa, consolidating its control over key value chains. The distribution of these pacts reveals the growing geopolitical rivalry surrounding access to and refining of strategic minerals.

Innovation in circular economy and recycling emerges as the third strategic pillar, where Europe seeks to establish global leadership. Early results are promising: the North Rhine-Westphalia pilot project has achieved recovery rates of 95% for critical materials from spent batteries, while VITO in Belgium has developed processes with efficiency exceeding 90% in recycling of strategic metals. These initiatives not only reduce reliance on virgin raw materials but also position Europe as a leader in advanced recycling technologies, a market projected to reach 25 billion euros by 2030.

“The Global Gateway Initiative transcends the traditional infrastructure approach to embrace a holistic vision that includes technology transfer, local capability development, and the setting of sustainable standards”

The Global Gateway Initiative, with an envisaged investment of 300 billion euros, represents the fourth pillar of Europe’s strategy. This program goes beyond traditional infrastructure to adopt a comprehensive approach that includes technology transfer, the development of local capabilities, and the establishment of sustainable standards. In Latin America, for example, the initiative supports the development of refining capabilities in the Lithium Triangle, aiming to create a more balanced and sustainable value chain. In Africa, projects focus on improving working conditions and environmental practices in cobalt extraction, promoting a more equitable model of collaboration.

However, implementing the CRMA could encounter significant barriers within Europe. In Spain, the lithium project in Extremadura has faced strong opposition from environmental groups such as Salvemos la Montaña, which warn about risks of groundwater contamination and biodiversity loss in the Valdeflores Valley (Cáceres). This case mirrors the dilemma between the need to secure essential raw materials and social pressure to protect the environment.

The effectiveness of Europe’s strategy will largely depend on its ability to coordinate action across multiple levels and stakeholders. Mobilizing substantial investments, estimated at more than €100 billion through 2030, will require a blend of public and private funding. Coordination among member states, especially in areas such as research and development or standardization of processes, will be crucial. Equally important will be the capacity to sustain public support by effectively communicating the strategic importance of these projects and their long-term sustainability benefits.

Spain: a pillar for European sovereignty in critical materials

Spain possesses a key geological and industrial potential to drive the European Union’s strategic autonomy in critical materials. The lithium deposit of San José de Valdeflórez, in Extremadura, with reserves exceeding 1.2 million tonnes, could meet up to 30% of Europe’s projected demand for 2030. Added to this is the construction of a gigafactory in Sagunto (València), with an investment of more than €3 billion. This project aims to integrate raw-material extraction with the production of advanced technological components, closing the value loop and strengthening Spain’s position in Europe’s industrial chain.

Moreover, regions with an established industrial base, such as Catalonia and the Basque Country, lead innovative initiatives that reinforce the country’s commitment to the circular economy and sustainability. Notable examples include the Basque Circular Hub, focused on recycling lithium batteries, and the Manresa Technological Center, specializing in recovering rare metals from electronic waste. These initiatives demonstrate how Spain can reduce its reliance on imports through cutting-edge technologies.

“With a strategic and coordinated approach, Spain is well positioned to become a key driver of Europe’s energy and technological transition”

Geopolitically, Spain plays a strategic role in building international alliances. Its historical ties with Latin America and its growing links with Africa position it as a natural bridge in international negotiations. Within European initiatives such as Global Gateway, Spain can act as an interlocutor to promote sustainable deals that balance access to resources with local development.

The challenge for Spain is to consolidate these advantages by building refining and manufacturing infrastructures that increase the value added of extracted resources and by ensuring a stable, attractive regulatory framework for investment. With a strategic and coordinated approach, the country is well placed to become a key engine of Europe’s energy and technological transition, while strengthening its leadership in innovation and sustainability.

Autonomy or dependence? The European transition in the face of global challenges

The geopolitics of critical materials has entered a decisive phase, as illustrated by Ukraine’s proposal to trade rare earths for U.S. military support or by the Trump Administration’s ambitions over Greenland. This new dynamic is reflected in statements by Trump’s National Security Advisor, Mike Waltz, who has made explicit the intention to “recoup costs” through partnerships centered on natural resources, signaling a fundamental shift in the United States’ approach to international aid. These episodes illustrate how the transition toward a green and digital economy is redefining global power dynamics, posing structural challenges for the European Union.

“The success of Europe’s ecological and digital transition will depend on its ability to balance industrial ambitions with sustainability and social cohesion”

In this sense, Europe’s response must be multidimensional, combining diversification of international alliances with the development of domestic capabilities. Expanding agreements beyond Canada and Australia to Latin America and Africa, promoting the circular economy, and building refining capabilities are essential elements of this strategy. At the same time, advancing high social and environmental standards, along with strengthening resilience to global disruptions, are crucial to building a distinctive European model.

The success of Europe’s ecological and digital transition will rely on its ability to balance industrial ambitions with sustainability and social cohesion. Spain, with its natural resources and emerging technological capacity, can play a central role in this transformation. The EU now has an opportunity to develop a new paradigm of strategic autonomy that combines economic resilience with global responsibility, thereby establishing a model suited to the challenges of the twenty-first century.

*This article includes information from the report on stocks of critical materials by the Observatoire de la sécurité des flux et des matières énergétiques, coordinated by IRIS with the collaboration of Enerdata and Cassini, and supported by the DGRIS of the French Ministry of the Armed Forces. Cassini contributes its expertise in geopolitical risk analysis and mapping.