Twenty-seven days after the Epic Fury operation against Iran, launched on February 28, 2026 by the United States and Israel, the Strait of Hormuz remains closed; thousands have died on all fronts; more than four million have been displaced, and Brent crude—the global benchmark for oil prices—has oscillated between 100 and 119 dollars after starting from 67 before the conflict. The International Energy Agency has described it as the greatest disruption of energy supply in history. However, analyzing this conflict solely as a regional war prevents understanding the dynamics that fuel it.

These dynamics operate at several simultaneous scales (the global competition among great powers, the power balances in the Middle East, and the physical geography of a 34-kilometer-wide strait) and only make sense when analyzed together.

Iran and Venezuela in the Context of the Sino-American Rivalry

Hover over the map to zoom. It shows the world’s energy dependencies on Hormuz and the alternatives China has developed to reduce its vulnerability, from land routes to ports and strategic infrastructures. | Map: Agenda Pública / Kartex

Iran’s war cannot be explained without what happened eight weeks earlier in Caracas. On January 3, 2026, the United States captured Nicolás Maduro. Each of these operations responds to its own motivations (in the case of Iran, nuclear proliferation and Israeli pressure; in the case of Venezuela, migratory policy and the democratic crisis), but both share an element worth highlighting. Iran and Venezuela are the two main crude oil suppliers to China outside the routes that the United States militarily controls. Iran supplied 13.5% of China’s maritime crude imports in 2025; Venezuela accounted for another 4%. In a period of about sixty days, roughly 17% of China’s oil supply has been interrupted by two consecutive American operations.

Taken together, this sequence carries strategic implications that go beyond each operation on its own. Nearly 40% of China’s imported oil transits Hormuz daily, and 80% of its maritime crude passes through the Malacca Strait. China’s dependence on maritime chokepoints, a constant concern in the strategic planning of the Chinese government for two decades, has ceased to be a hypothetical scenario.

“Japan depends on Hormuz for 75% of its imported crude, South Korea for 68%, India for about half of its oil and more than half of its gas”

The global map makes this double dynamic visible. On one hand, the vulnerability of Asian economies. Japan depends on Hormuz for 75% of its imported crude, South Korea for 68%, India for about half of its oil and more than half of its gas. China itself, despite its diversification strategy, continues to depend on Hormuz for 25% of its LNG. On the other hand, the response the Chinese government has been building for years to reduce that exposure. Land pipelines from Siberia, Central Asia and Myanmar, ports integrated into the Belt and Road Initiative, and crude oil reserves estimated at more than 1,200 billion barrels, offering more than one hundred days of autonomy. Added to this is a factor that many analyses overlook. More than half of the cars sold in China in 2025 were electric, and the country’s electric vehicle fleet already exceeds 30 million units. Nomura estimates that the oil transiting Hormuz already accounts for only 6.6% of total Chinese energy consumption. The energy transition is reconfiguring vulnerability balances among the great powers, and this war helps make that evident.

China’s stance in the conflict reflects that ambivalence. Pekín has condemned the attacks, but has not provided military aid to Tehran, despite a 25-year strategic partnership and more than $100 billion in accumulated investments. The Xi–Trump summit, initially planned for late March, has been postponed for several weeks because of the conflict, suggesting that China prefers to negotiate with the United States from a position of patience rather than risk its bilateral relationship to defend a partner under military pressure. China’s relationship with Iran has always been more commercial than ideological, and this war has laid that bare. At the same time, various analyses point to Chinese restraint not equaling indifference, but rather a long-term calculation in which the wear and tear of the United States in the Gulf, the growing dependence on a weakened Iran on China, and the possibility of leading post-conflict reconstruction could end up strengthening China’s position in the region without the need for direct confrontation.

The war also has a dimension that transcends hydrocarbons. The Middle East produces 24% of the world’s sulfur, essential for processing copper and nickel, and 9% of the Gulf Cooperation Council’s primary aluminum. Large volumes of fertilizers remain stranded near the Strait. China has restricted its own fertilizer exports. The conflict not only alters energy flows but also affects the supply chains underpinning both the green transition and Western defense industry.

“According to BBVA Research estimates, the conflict could shave two tenths off Spain’s GDP growth and add three tenths to inflation in 2026”

For Spain, whose direct dependence on Hormuz is marginal (Qatar accounts for barely 1.7% of gas imports, with Algeria, the United States, and Russia as the main suppliers), the impact arrives through price, not supply. LNG is traded on a global market, and the European gas price index (the Dutch TTF) has risen from about €30 per megawatt-hour in February to peaks above €60, dragging electricity prices. Gasoline 95 has surpassed €1.60 per liter. According to BBVA Research estimates, the conflict could subtract two tenths from Spain’s GDP growth and add three tenths to inflation in 2026, a contained effect, but one that compounds against a European economy still absorbing the consequences of the war in Ukraine.

A Coalition with Two Logics Against a Weakened Iranian Axis of Resistance

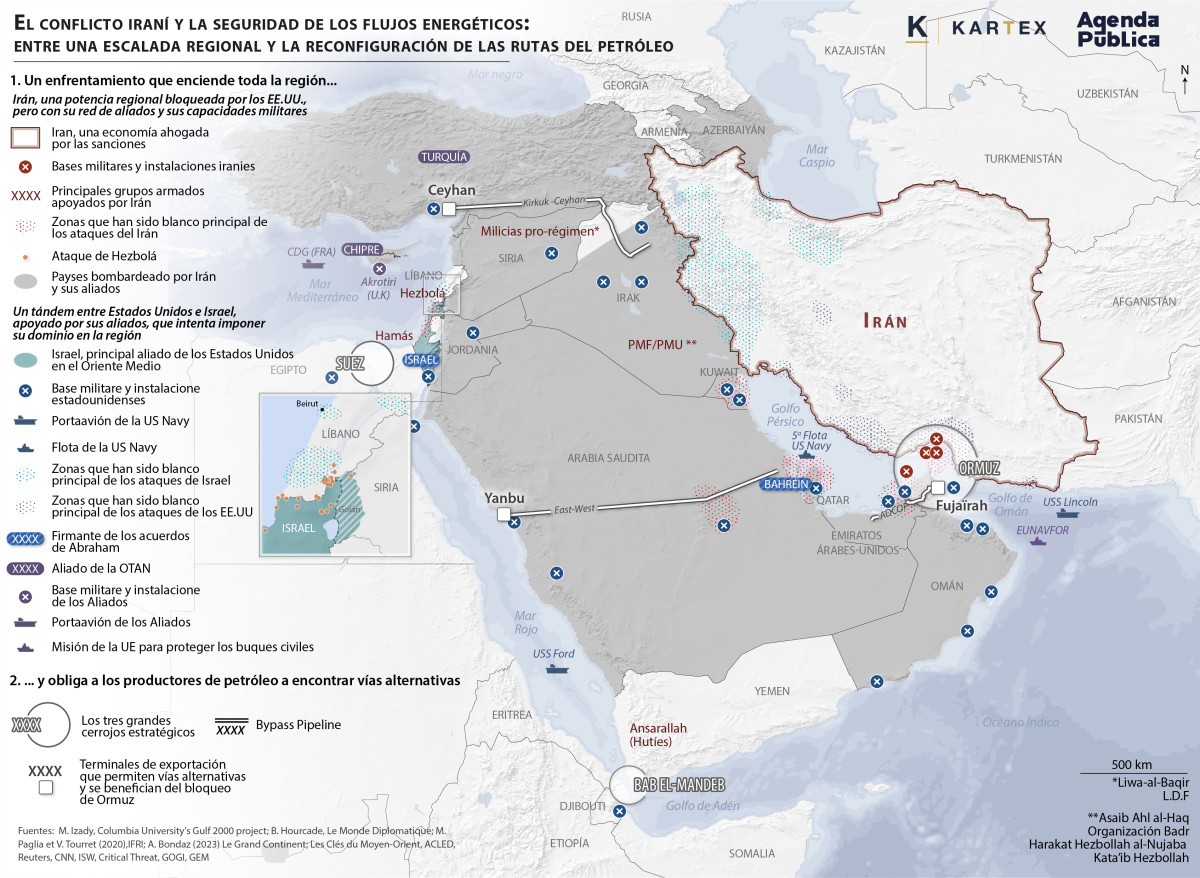

Hover over the map to zoom. It shows the regional actors of the conflict, the main lines of attack, the military bases, and the alignments that explain the war at the Middle East level. | Map: Agenda Pública / Kartex

If the global scale helps understand the role of the Sino-American rivalry as a structural factor, regional analysis shows that the motivations of the two members of the attacking coalition differ significantly, which conditions both the course of operations and any future negotiation prospects.

The regional map helps identify the main actors, lines of attack, and regional alignments. For Israel, this war has an existential dimension. Netanyahu has invoked the need to eliminate the Iranian nuclear threat and has overseen a campaign of targeted killings against the regime’s leadership. Khamenei was targeted in the early bombings, Larijani on March 17, and Intelligence Minister Khatib the following day. At the same time, Israel has leveraged the context to launch a ground offensive against Hizbullah in Lebanon and attacked the South Pars gas complex on March 18, a decision that provoked explicit irritation from Trump. Israel’s ambition goes beyond neutralizing the program and aims to dismantle the network of alliances Iran has built in the region over two decades. It is worth bearing in mind that Israel faces legislative elections slated for October 2026, with the possibility of a snap poll in June or July, which introduces a domestic political factor in waging the war. For the United States, however, the objectives are of a different nature. Trump explicitly invoked a regime change on February 13, at a moment when Iran was undergoing the greatest internal crisis since the 1979 revolution, with thousands of protesters on the streets throughout January 2026 and a crackdown that weakened the regime’s legitimacy even further. The strategic framework of the operation connects with containing China and reaffirming U.S. control over Gulf energy routes. Yet the divergence between the two agendas —which regional analysis had anticipated— has become visible in recent days. While Israel intensified attacks on Iranian energy infrastructure and launched a ground invasion in southern Lebanon, Trump announced on March 23 a five-day pause in bombing Iranian power plants, citing ‘productive conversations’ with Iran, which the Iranian government has categorically denied.

“The Iranian allies network has not functioned as a coordinated device, but as a set of actors with their own agendas and uneven degrees of freedom”

The so-called Iranian “axis of resistance,” which both the theocratic rhetoric and much of Western strategic literature presented as a cohesive regional threat, had shown signs of fragility since Israel’s offensive on Gaza in October 2023. Iran’s inability to protect Hamas, Hizbullah’s gradual degradation through selective Israeli operations during 2024 and 2025, and the détente between the Houthis and Saudi Arabia had been eroding the credibility of this deterrence architecture before the current war began. Epic Fury Operation abruptly confirmed that fragility. Hizbullah opened a second front on March 2 with rockets on Haifa and the Upper Galilee, which first led to ground operations by Israel south of the Litani and, since March 16, a ground invasion that has raised the Libyan/Lebanon toll to over 1,000 dead and about a million displaced, nearly a fifth of the population. Hamas remains in a fragile ceasefire since January 2025 that the war has frozen. As for the Houthis, their position has evolved in recent days. After staying on the sidelines for the first three weeks of the conflict, the movement formally declared its entry into the war on March 22, though it has not launched attacks to date. This statement without immediate action confirms the logic at work since the conflict began. The Iranian network of allies has not functioned as a coordinated device, but as a set of actors with their own agendas and varying degrees of freedom, whose capacity to project depended on a deterrence that, tested by direct intervention, has not produced the joint response the Iranian government needed.

Gulf countries, for their part, find themselves in a particularly complex position, trapped between their historic rivalry with Iran and their need for stability to protect their economies and their international prestige. Iran has launched reprisals against the six Gulf Cooperation Council states. The Emirates have borne the brunt, with more than 350 ballistic missiles and 1,800 drones received. The Ras Laffan LNG complex in Qatar, the world’s largest, has lost 17% of its capacity after the March 19 attack, with damages that QatarEnergy estimates to be irreparable for three to five years. Israel’s strike against South Pars, the world’s largest gas field shared by Iran and Qatar, has strained tensions between Qatar and the coalition. These same states host the bases from which the coalition operates, so the military presence intended to protect them is what makes them targets.

“President Sánchez pronounced a televised ‘No to War’ on March 4, prohibited the use of the Rota and Morón bases for operations against Iran, and recalled the ambassador to Israel”

Europe has dissented, though with varying intensities. No NATO ally participated in the initial attacks nor was consulted beforehand. Spain has stood out as the continent’s most vocal critic. President Sánchez delivered a televised “No to War” on March 4, banned the use of the Rota and Morón bases for operations against Iran, recalled the ambassador to Israel, and rejected Macron’s proposal for a naval mission in Hormuz. The United States administration responded by threatening to cut bilateral trade. The nearly 300 Spanish troops in the NATO mission in Iraq have been evacuated to Turkey in a move the defense minister described as “very complex.” It is a stance that evokes the 2003 precedent, but in a context where European strategic autonomy is more pressing than then.

A 34-Kilometer Geography That Paralyses the Global Economy

The third scale shift places the analysis in the concrete geography of the Strait of Hormuz, a stretch of merely 34 kilometers between Iran and Oman, crossed by two navigation corridors of 3.5 kilometers each that border Iranian territory. The islands of Qeshm, Larak, and Abu Musa, controlled by Iran, lie along these transit corridors, giving Iranian forces a dominant position over commercial navigation.

The local picture reveals the density of infrastructure concentrated in this compact space. The Gulf’s major fields (Ghawar, the world’s largest oil field, Burgan, and the South Pars/North Dome giant, shared by Iran and Qatar) feed a network of export terminals whose production leaves almost exclusively through this corridor. The military bases on both sides of the strait are deployed with a proximity that explains both the effectiveness of the closure and the difficulty of reversing it.

“This is a clear example of asymmetric warfare, where a player with limited naval capabilities can paralyze the planet’s main energy artery with costs far lower than the damage they inflict”

The strait has effectively been closed since March 1, something that had not happened since the so-called “tanker war” during the Iran-Iraq conflict in the 1980s, albeit on an unprecedented scale. The mechanism is significant in itself. It is not a conventional naval blockade, but a combination of low-cost drones, selective attacks against commercial vessels, and mining of the seabed. After the attack on the tanker Skylight, insurers canceled marine coverage and major shipping lines suspended all transits. Only about twenty tankers have crossed since the war began, compared with more than a hundred ships daily under normal conditions. Thousands of vessels remain stranded in the region. It is a clear example of asymmetric warfare, where a player with limited naval capabilities can paralyze the planet’s main energy artery with costs far lower than the damage they cause.

The figures are a measure of the disruption. The usual Hormuz flows amount to about 15 million barrels of crude per day, 31% of the world’s maritime oil trade, plus 20% of global LNG. The coordinated release of 400 million barrels of strategic reserves by the 32 member countries of the International Energy Agency, the largest such operation ever conducted, nevertheless equals less than five days of the interrupted volume. Of the six major Gulf exporters, only Saudi Arabia and the United Arab Emirates have alternative pipelines that allow some of their production to be routed without passing through Hormuz (the Saudi Petroline to the Red Sea and the Emirati ADCOP pipeline to Fujairah, in the Gulf of Oman). Iraq, Kuwait, Qatar, and Iran lack overland alternatives and depend entirely on Hormuz for export. The combined maximum capacity of these pipelines is about 9 million barrels per day versus the 20 million that used to transit, a gap that no existing infrastructure can fill.

The war has also highlighted a vulnerability that transcends energy. More than 400 desalination plants line the coasts of the Persian Gulf, produce more than half of the world’s desalinated water, and supply drinking water to around 100 million people. Kuwait relies on desalination for 90% of its water, Qatar for over 99%. Iran, which despite its own water stress relies mainly on rivers and inland aquifers for water, does not depend on coastal desalination infrastructure. Its Gulf neighbors, however, cannot do without it. This asymmetry gives the Iranian government coercive leverage that goes beyond purely military means, because an attack on these facilities would not only destroy infrastructure, but threaten the very habitability of Gulf territories. Direct attacks on desalination plants have been limited so far, but the risk of escalation in this direction remains one of the gravest humanitarian dangers of the conflict.

A Global Era Change, a Regional Context with no Clear Diplomatic Exit

What the analysis at different scales reveals is that only by articulating these three levels can we understand a conflict like the one we are living through. It is the first open conflict in which the Sino-American rivalry directly projects onto energy routes, critical mineral supply chains, and the security architecture of an entire region. The Venezuela–Iran sequence in barely two months points to a US strategic logic aimed at reconfiguring global energy flows in a context of direct competition with China for control of supply routes. Yet this war, conceived in part to curb China’s position, could end up strengthening the trend it seeks to contain. China’s energy resilience, with its reserves, land routes, and progress in electrification, gradually reduces the effectiveness of a strategy based on controlling sea routes. It seems we may be facing one of the last conflicts in which oil serves as a principal geopolitical instrument, and the first in which a major power’s energy transition tangibly alters the strategic equation of a war.

“A few dozen countries have signed declarations in favor of reopening Hormuz, but no naval escort operation has materialized”

In the Middle East, the outlook offers limited short-term room for diplomatic resolution, though the past week has introduced contradictory signals. The Iranian “axis of resistance” has shown fragility in direct confrontation. Gulf states watch their energy infrastructure suffer damage that will take years to repair. The Saudi-Israeli normalization, a cornerstone of the diplomatic architecture the Biden administration promoted before the war, has been suspended indefinitely. On March 23, Trump announced a five-day pause in attacks on Iranian energy infrastructure, claiming there were “productive conversations” to end the conflict. Iran denied any direct negotiations, though acknowledged receiving American proposals through mediators (Turkey, Egypt, and Pakistan). It is too soon to know whether this window will lead to a real process or close in the coming days. What is clear is that the divergence between Israel and the United States, which regional analysis had anticipated, has manifested openly. Israel continued attacking targets in Iran and Lebanon during the U.S. pause. A few dozen countries have signed declarations in favor of reopening Hormuz, but no naval escort operation has materialized.

Spain, physically distant but politically exposed, has chosen to oppose military intervention. Its dependence on Hormuz is marginal, but its vulnerability to the global energy price is total. Its decision to publicly oppose the war, at a moment when transatlantic consensus is weaker than it has been since 2003, reflects both a national stance and a broader fracture within Western democracies regarding unilateral use of force.

Its repercussions extend from Asian energy security to European gas markets, and redefine the parameters of global geostrategic competition for the coming decades.