The race for critical minerals has become one of the structural axes of rivalry among the great powers. The second Trump Administration has accelerated it with an unprecedented turn, deploying a diplomacy that conditions American security commitments on access to strategic resources. The Washington Agreements between the Democratic Republic of the Congo and Rwanda, signed on December 4, 2025, are its most recent expression.

“The power that shaped the postwar international order is now altering the rules it itself established, driven by its own external dependencies”

The United States mediates in a conflict that has destabilized eastern Congo for three decades, but ties its involvement to access to cobalt deposits, which account for 70% of global production. A day earlier, the European Commission approved the RESourceEU Plan, a response that evidences the distance with Washington in capacity to act. This article examines the structural roots of this competition and its recent evolution, with special attention to the rivalry between the United States and China, the European Union’s institutional responses and the limitations of the Spanish case.

The American Imperial Paradox: Dependence in the Era of Hegemony

The power that shaped the postwar international order is now altering the rules it itself established, driven by its own external dependencies. This is the American imperial paradox. Of the sixty minerals that the United States Geological Survey classifies as critical on its 2025 list, forty exhibit import dependence above 50%; for twelve of them, dependence is total. China, for its part, dominates 91% of global refined rare earths according to the International Energy Agency, in addition to the production of gallium, germanium and processed graphite, essential inputs for advanced semiconductors and next‑generation batteries. China’s advantage is not solely extractive. Its refining plants operate with margins that neither the United States nor the European Union can replicate without sustained subsidies.

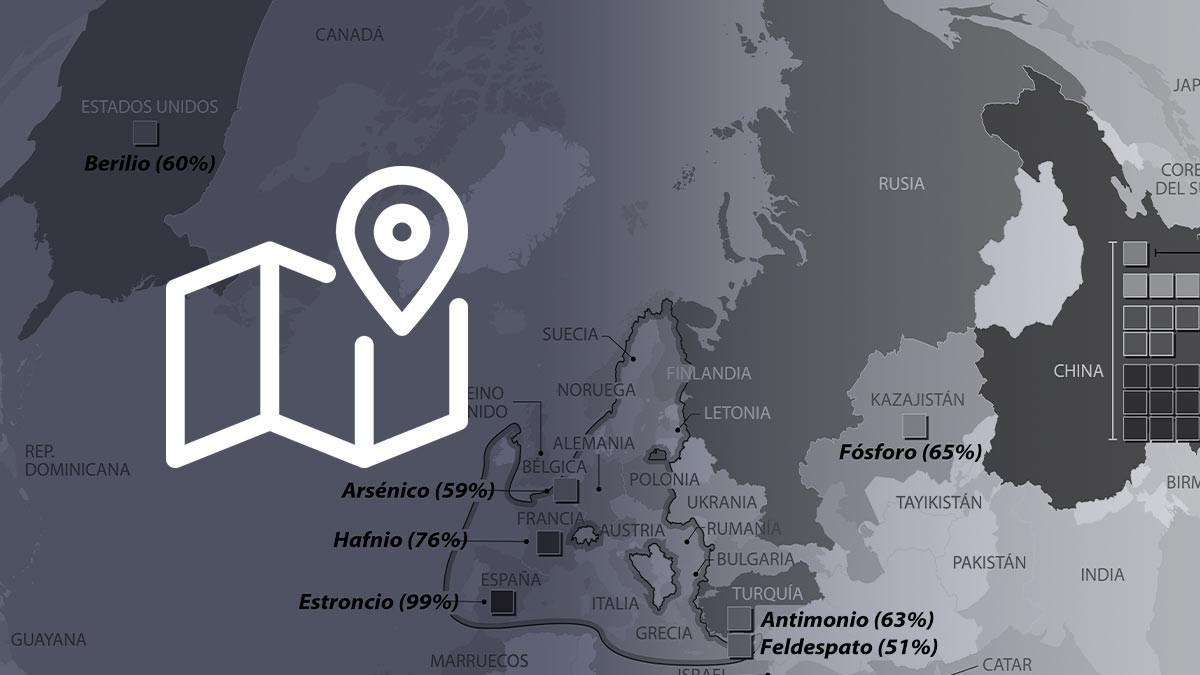

Pulse to zoom. The green countries indicate minerals for which the United States relies on imports by more than 50%, while the bars identify cases where a single supplier concentrates most of the supply. The map shows that the main U.S. vulnerability lies in the concentration of supply and in processing stages, more than in the geological availability of resources. Map: Thomas Cattin, Cassini Spain.

This vulnerability has internal roots. The globalization that the United States fostered gradually hollowed out its manufacturing base, including the mining and industrial infrastructure needed to process these resources. According to the Bureau of Labor Statistics, manufacturing employment fell from 19.6 million workers in 1979 to 12.8 million in 2023. In 2015, Molycorp, the only rare‑earth processing plant on U.S. soil, closed due to bankruptcy, unable to compete with Chinese prices. As this erosion advanced, budget priorities after 9/11 privileged military interventions in the Middle East. China, by contrast, systematically invested in industrial development and in controlling the supply chains of strategic raw materials.

“Historical alliances, forged in the Cold War and maintained through decades of hegemony, are now reconfiguring around supply chains”

That is the rationale behind the shift in U.S. foreign policy. Protectionism, marginal for decades in a liberal‑free trade consensus, has moved to the center of trade policy. Historical alliances, forged in the Cold War and maintained through decades of hegemony, are being reconfigured around supply chains that will determine who dominates the industries of the future.

The Reshaping of U.S. Strategy: Between Continuity and Unilateralism

Critical minerals did not crystallize as a geopolitical issue until the 2010s, when they began to condition industrial competitiveness and strategic autonomy of the great powers. A turning point was China’s decision to restrict rare-earth exports in 2010, cutting quotas by 40% in the context of the dispute with Japan over the Senkaku Islands. China then demonstrated that it could use the supply of raw materials as a lever of pressure. Since then, reducing this vulnerability has become a bipartisan consensus in Washington. The National Defense Stockpile, created in 1939 and largely overlooked after the Cold War, regained prominence. Congress began commissioning studies on supply vulnerability for the defense industry.

The consensus on the substance has coexisted with notable differences in form. Beyond electoral cycles, what structures U.S. policy since 2010 is the perception of a long‑range rivalry with China for access to the inputs that underpin its industrial and military base. Trump’s first term (2017‑2021) resorted to executive orders urging federal agencies to identify critical dependencies and accelerate domestic production, reaching in 2020 to declare a national emergency that enabled defense funds for mining projects. The Biden Administration (2021‑2025) favored the legislative route, harder to reverse, and multilateral coordination. The CHIPS and Science Act and the Inflation Reduction Act jointly mobilized more than $600 billion for semiconductors, clean energy, and reindustrialization. The Minerals Security Partnership, launched in 2022 with Japan, South Korea, Australia, and the European Union, sought to articulate a coordinated response to the Chinese dominance.

“The new wave of executive orders authorizes extraction on federal lands, with Alaska as a priority. The distinctive feature of this stage is the simultaneous deployment of trade pressure and transactional diplomacy”

The second Trump Administration marks a break with multilateralism, not with the underlying conflict. The new wave of executive orders authorizes extraction on federal lands, with Alaska as a priority. The distinctive feature of this stage is the simultaneous deployment of trade pressure and transactional diplomacy. The so‑called “Liberation Day,” in April 2025, imposed a base tariff of 10% and escalated duties up to 50% on economies with the largest bilateral deficits, without distinguishing between adversaries and allies. Pressures on Denmark over Greenland, the inclusion of access to Ukrainian minerals in the negotiations over the conflict, or the Washington accords with the DRC and Rwanda respond to this same logic.

Central Asia: a Laboratory for the China Rivalry

The current competition for critical minerals cannot be understood without taking into account the strategy China has deployed over three decades to secure access to resources located outside its borders. Chinese state-owned enterprises and private Chinese consortia have acquired stakes in mining operations, financed transportation infrastructure, and signed long-term purchase agreements across three continents. In the Democratic Republic of the Congo, Chinese firms control fifteen of the seventeen cobalt operations and dominate 70% of the mining sector.

In the South American lithium triangle, the Chinese CATL, the world’s largest battery producer for electric vehicles, leads a $1.4 billion consortium in Bolivia, while other firms expand operations in Argentina and Chile. The Trump–Xi summit in Busan, in October 2025, underscored how far this accumulation of positions has become bargaining power. China achieved the temporary suspension of controls in exchange for a reduction in the US tariff from 57% to 47%.

“Over the past two decades the Chinese government has woven new dependencies through investments in connecting infrastructure, stakes in extractive firms, and preferential trade agreements”

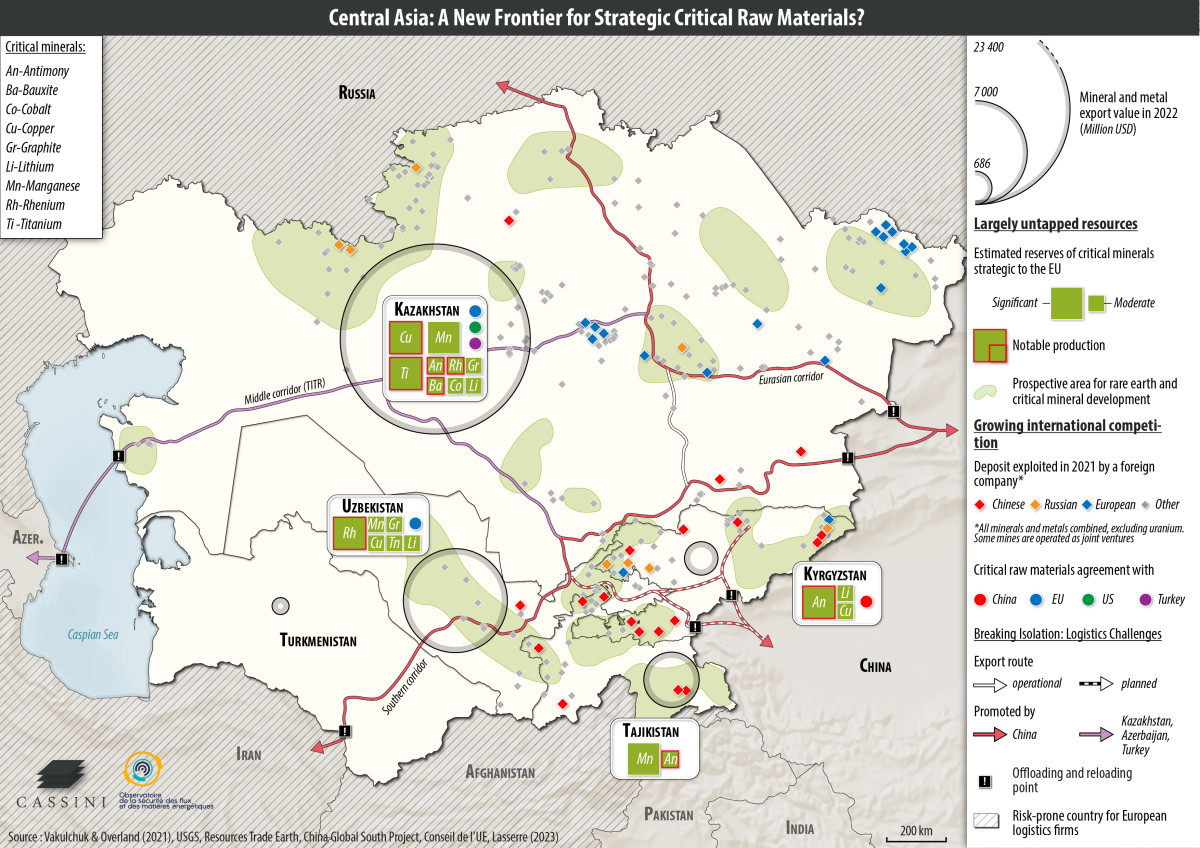

China’s reach extends across continents. Central Asia offers a view of how these rivalries play out at a regional scale. It is a landlocked region, bordered by Russia, China, Iran and Afghanistan, producing 19 of the 34 minerals that the European Union lists as critical. The five post-Soviet republics have historical ties to Russia, but in the last two decades the Chinese government has woven new dependencies through investments in connecting infrastructure, stakes in extractive companies, and preferential trade accords. The railway linking China, Kyrgyzstan and Uzbekistan stands as the most emblematic project of this projection toward what China regards as its strategic periphery.

Pulse to zoom. The map overlays zones with significant reserves, mining operations controlled by foreign players, and major transportation corridors. This combination shows that the strategic value of Central Asia lies not only in its resources but in the control of the infrastructures and the routes that enable its integration into global supply chains. Map: Thomas Cattin, Cassini.

The C5+1 summit in November 2025, which brought together Trump with the leaders of Kazakhstan, Uzbekistan, Kyrgyzstan, Tajikistan and Turkmenistan, represents an attempt to contest this influence. Total commitments reached $130 billion, including a tungsten joint venture in Kazakhstan. The discovery of the “New Kazakhstan” deposit in Karaganda, announced in April 2025, reinforces the region’s strategic interest, with proven reserves of one million tonnes of rare earths. Current trade flows, however, show a different reality. In 2023, Kazakhstan exported critical minerals worth $3.07 billion to China and $1.8 billion to Russia, compared with just $544 million to the United States. A structural dependence hard to reverse in the short term.

A Europe Moving at a Different Pace

The European Union was left out of the Busan negotiations, a bilateral agreement that directly affects its interests. Its position in the competition for critical minerals is marked by an import dependence exceeding 90% for a dozen strategic materials, including boron, niobium, titanium, magnesium, refined lithium and rare earths. In permanent magnets, essential for electric motors and wind turbines, China’s share of dependence reaches 98%.

“China’s 2010 restrictions had already shown the risks of concentration of supply, but Europe’s response took more than a decade to materialize”

This vulnerability is not new. China’s restrictions of 2010 had already highlighted the risks of supply concentration, but Europe’s response took more than a decade to materialize. It was the energy crisis arising from the Ukraine war that accelerated the shift in focus, by showing that external dependencies could become strategic vulnerabilities. The European Critical Raw Materials Act (CRMA), in force since May 2024, established binding targets for 2030 for the first time. Ten percent of annual consumption must come from European extraction, 40% from domestic processing, and 25% from recycling. No third country may supply more than 65% of any strategic raw material.

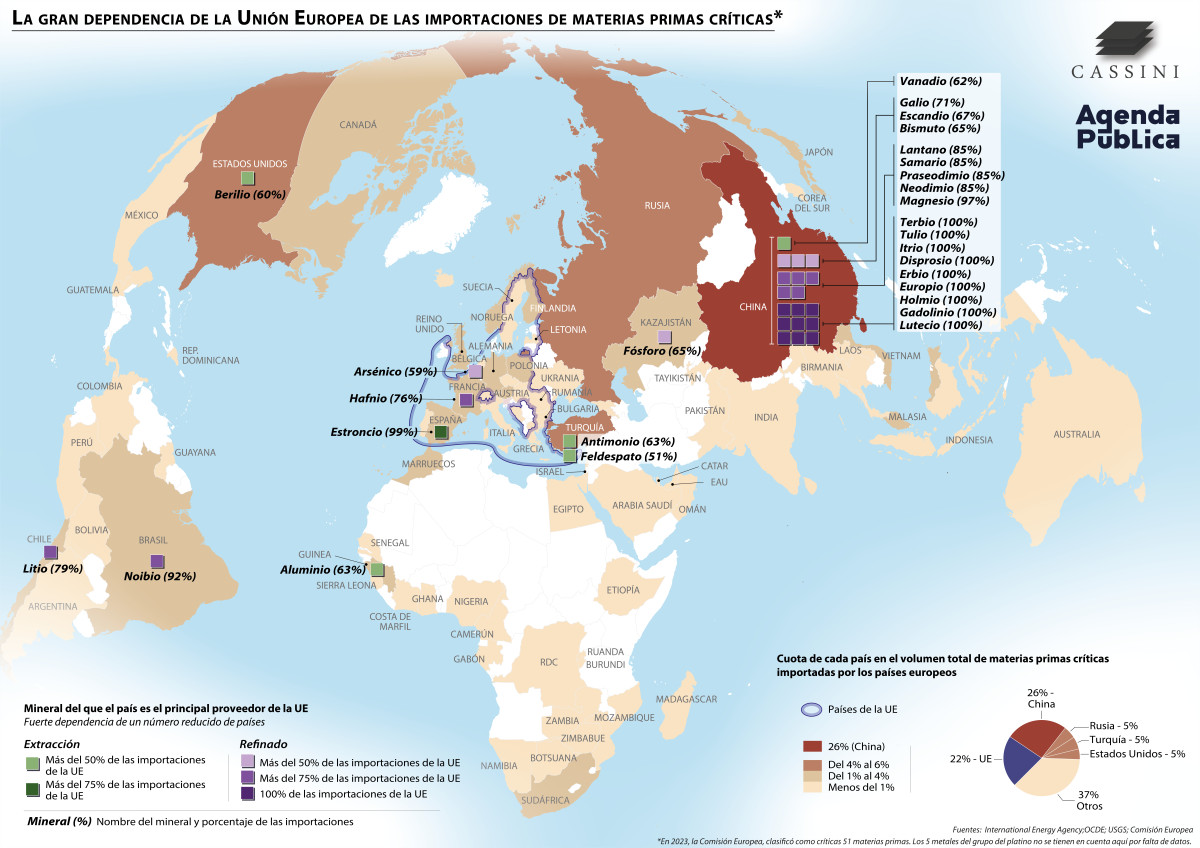

Pulse to zoom. Map: Cassini.

The RESourceEU Plan, approved on December 3, 2025, seeks to translate these objectives into operational capacities. It mobilizes €3 billion over twelve months. Its main instruments are a European Center for Critical Raw Materials, to be operating from 2026 and modeled on Japan’s JOGMEC, a joint procurement platform to aggregate demand of the member states, a pilot strategic storage program and restrictions on the export of permanent-magnet scrap. On the external front, the strategy rests on fifteen partnerships with producing countries, the most recent with South Africa in November 2025.

These figures, however, reveal the magnitude of the gap. The 3.0 billion euros in Europe pale next to the 130 billion pledged by the United States in Central Asia or the volumes of Chinese investment in Africa and Latin America. And the main challenge lies in timing. Developing a mining operation from exploration to production requires ten to fifteen years in the European regulatory context. The 2030 targets will depend on projects already in advanced stages and on the ability to accelerate procedures without eroding the environmental standards that the Union itself promotes as its hallmark.

The Spanish Case

European objectives depend on what happens within the member states. Of the 47 projects selected by the European Commission in March 2025, seven are located in Spain. Two are tungsten, two lithium, one cobalt–nickel, and two copper and recycling. But unlike Portugal, which already exports lithium, or the Nordic countries with established mining infrastructure, Spain lacks operational capacity despite its historical tungsten tradition.

“Spain has reserves of 32,000 metric tons according to the USGS and hosts two of the three European projects recognized as strategic”

The tungsten represents the most concrete opportunity. Spain possesses reserves of 32,000 metric tons according to the USGS and hosts two of the three European projects recognized as strategic. The El Moto deposit, in Ciudad Real, could supply 20% of European demand in its first phase. Lithium presents a more complex picture. The Cáceres project, the second-largest European hard rock lithium deposit, is conditioned by strong citizen mobilization since 2017, aggravated by its proximity to the historic center designated as a World Heritage site. The collapse of international prices, which fell from $78,000 to under $15,000 per ton, has added economic uncertainty to local opposition. In rare earths, European studies conclude that there are no economically viable deposits on the Iberian Peninsula.

To these limitations, regulatory uncertainty is added. The 2025‑2029 Action Plan, the first national program for mining exploration in half a century, lacks a specific budget. The mining competences, distributed between the State and the autonomous communities, generate a fragmented framework that slows procedures. All told, the main challenge is not extraction but industrial. Without processing capacity, Spain could be limited to exporting raw material without adding value.

Strategic Autonomy: an Uncertain Horizon

The issue of access to critical minerals has become the backbone of both foreign and industrial policy among the major powers in the 21st century. For the United States, what is at stake is the ability to maintain its industrial hegemony in a context it helped create. The interdependence that for decades was presented as a hallmark of successful globalization now reveals itself as a structural vulnerability, and correcting it demands timelines that political polarization and shifting priorities between administrations hardly guarantee. China, by contrast, has demonstrated what long-term planning looks like. Three decades of sustained investment in refining capacity, strategic acquisitions abroad, and the development of connecting infrastructures have allowed it to master not only extraction but the entire value chain, from ore to finished component.

“For the European Union, the challenge is to reduce decades of accumulated dependencies in a context where the Trump administration’s unilateralism weakens its negotiating position”

For the European Union, the challenge is to reduce decades of accumulated dependencies in a context where the Trump Administration’s unilateralism weakens its negotiating position. The war in Ukraine has added urgency to the diagnosis, while China continues to control the inputs that Europe’s green transition needs. The CRMA and the RESourceEU Plan represent significant institutional advances, but their success will depend on the capacity to translate financial commitments into operational industrial capabilities at the speed demanded by the geopolitical context. The Spanish case illustrates the difficulties of translating this at a national scale. The present moment offers real opportunities in tungsten and, with more difficulty, in lithium. But administrative inertia and fragmented competencies threaten to close the window before it can materialize. The country needs not only to speed up procedures but to decide whether its aim is to export raw material or to capture the value of processing where value is added. And it must do so in a context of political instability and with a limited tradition of strategic thinking as a State.

Globally, all signs point to the persistence of a high‑intensity competition for access to critical minerals, with episodes of escalation and détente determined by the dynamics between the United States and China. Consequently, strategic autonomy requires sustained investments, stable regulatory frameworks, and a long‑term vision that transcends electoral cycles. Yet autonomy is also a matter of self-perception. Europe will not be able to act as a power in this field while it continues to conceive itself as a regulatory space or a market rather than as an actor with its own geopolitical project in the global race for resources.

This article incorporates information from the report on strategic stocks of critical materials by the Observatoire de la sécurité des flux et des matières énergétiques, coordinated by IRIS with the collaboration of Enerdata and Cassini, and supported by the DGRIS of the French Ministry of the Armed Forces.